The year-on-year increase in price (13% in 2019, according to the National Bank of Poland) has not yet tempered the enthusiasm of buyers. Developers are not stopping to introduce new investments on the market, but still find it difficult to keep up with the heated demand. One of the main obstacles is the increasingly acute lack of attractive land on which to launch the construction process efficiently. The rapid increases are also boosted by the prolonged periods during which companies have to wait for the required administrative decisions.

Limited availability of land causes companies to consider new locations

The best-placed companies are those developers which have succeeded in accumulating solid land banks to ensure that they can operate freely for the next few years. However, the rapid pace of sales and the related introduction of new projects on the market forces them to study the market constantly and to supplement depleted resources with new land. Not all companies enjoy this luxury. Some have to purchase plots of land on an ongoing basis in order to be able to continue their operations smoothly. Competition for land in large cities, and in Warsaw in particular, is intense. As a result, the prices expected by landowners exceed the levels acceptable to buyers. For some development companies the solution may be to expand into new markets. Whereas the residential property markets of several major cities are monitored on an ongoing basis by various agencies: research companies, property agents, etc., the remaining cities are extremely rarely subject to detailed research, to say nothing of benchmarking. It is, therefore, difficult to determine quickly and objectively which of these markets would be worth considering. Which cities should be taken into account when planning housing investments, and in which is it worthwhile to consider staying for a longer period of time. Conversely, should companies be wary of them instead? The answers to these questions are not at all obvious.

Assessment of 30 largest Polish cities in terms of their attractiveness to housing investors

A comprehensive evaluation of the attractiveness of individual centres in terms of residential investments against the background of a market created by the 30 cities included in the analysis constituted the raison d’etre for a study prepared by PMR. The report, entitled: “Residential investments in Poland. The ranking of the attractiveness of the 30 largest cities” scrutinises a broad group of cities and assesses them in terms of development prospects in the context of residential investments.

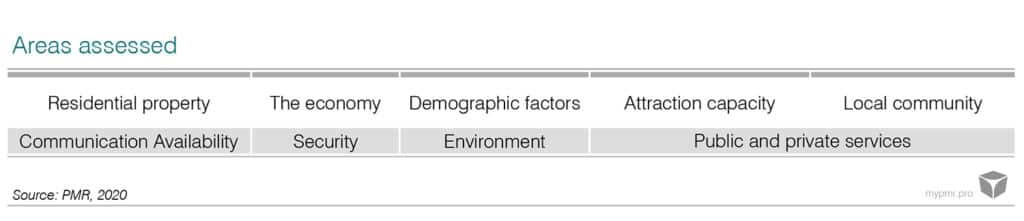

What aspects have been analysed? Nine areas were selected which, in the opinion of the authors of the report, have the strongest impact on the potential of housing construction. After this, within each of these, several sub-areas were identified, taking various aspects of a given issue into account. The sub-categories were characterised by means of selected indicators. In total, over 90 indicators were collected and analysed. The sources of the data were both public statistics and data presented by public bodies, central offices, industry-specific organisations, etc. In the arena of “attractiveness”, an additional review of publicly available rankings developed by institutions, foundations, companies and similar entities was carried out.

What is the result of the analysis?

The result of the analysis is the final ranking, along with detailed rankings for the 9 areas in question. During the calculation of the final ranking, individual areas were given weights which, in the opinion of the authors of the study, correlate with the strength of the influence on the attractiveness of housing construction. The assessment should not be seen in absolute terms, as it is a reference to the comparative group. The final ranking indicates cities which have better development prospects for residential investments in comparison with all cities surveyed and those whose outlook is less positive.

The ranking does not state directly where the profitability of developer investments lies, where it will reach its zenith or where the developers will sell most apartments. It does not compare a developer’s investment cost with the sales price, availability and cost of land, etc., which, given their nature, are variable and should be constantly monitored. Furthermore, they depend largely on individual knowledge and the degree of penetration of the local property market for each developer, along with the negotiating position, availability of capital, etc., which are inherently variable and should be constantly monitored.

The ranking presented is, however, a tool which makes possible a synthetic assessment of the city’s attractiveness in terms of residential investment potential in comparison with other centres. It enables the identification of both their strengths and weaknesses, and also facilitates the investor’s work in the preparation of strategies and long-term development plans. It is an appropriate starting point for further analyses based on data, not least because a detailed database is attached to the report, in which 92 analysed indicators were collected.

More detailed information may be found in the final ranking and partial rankings in the PMR report entitled: “Housing investments in Poland. Ranking of attractiveness of the 30 largest cities”.

AUTHOR

Szymon Jungiewicz

Construction Business Unit Director

MEDIA CONTACT

marketing@pmrcorporate.com

Recent posts

PMR’s report: Poles cut down on expenses but fashion does not come first

PMR’s estimates indicate that in 2022 the market will record growth again, mainly on the back of increased demand for…

PMR: PLN 58bn online sales of services in 2022

Data from the latest PMR report “Online retail of services in Poland 2022. E-commerce market analysis and development forecasts for…

PMR: Record-breaking cosmetics market growth in 2022

PMR forecasts that in 2022 the cosmetics market in Poland will grow by 6.1% YoY, to around PLN 27.7bn. This…

PMR Hospital Outcomes Index highest for private hospitals

The situation on the hospital market over the last 10 years was at its worst in autumn 2020, according to…

PMR: Ready-to-eat meals market in Poland is stable in difficult times

The ready-to-eat meals market in Poland is growing rapidly, being in a relatively early phase of development. In 2021, this…

PMR: Value of pharmaceutical distribution in Poland reached PLN 56bn in 2021

According to the latest PMR report “Distribution on the pharmaceutical market in Poland 2022. Market analysis and development forecasts for…